The Hidden Years of Inception Stage

Inception, Incorporation, Acceleration

TLDR: Founders & LP’s rarely understand that the journey of building a great company can involve up to three years of work before an early stage VC will get involved.

I’m pretty outspoken about the misconceptions in venture capital over what early stage investing truly is.

Many firms brag about being the first check in, backing founders earlier than anyone else, but representing their work that way is both a disservice to founders and to LP’s.

For founders, it encourages them to attempt to fundraise before they’re ready and in turn distracts them from doing what matters—talking to customers and building.

For LP’s, it gives the perception that these investors somehow have unique deal flow and asymmetric access to the best founders and companies. This is true of the best funds, and access to the second-time known-quantity founders, but the point I’m trying to make is that “first check in” is also claimed by the masses of VC’s who don’t truly support founders at inception, or even acceleration.

And while I don’t think it’s a malicious claim, it is disconnected from the reality of what it takes a founder to go from zero to one.

I was talking about this with Peter Walker from Carta recently, who is consistently publishing some of the most interesting data for early stage founders and VC’s.

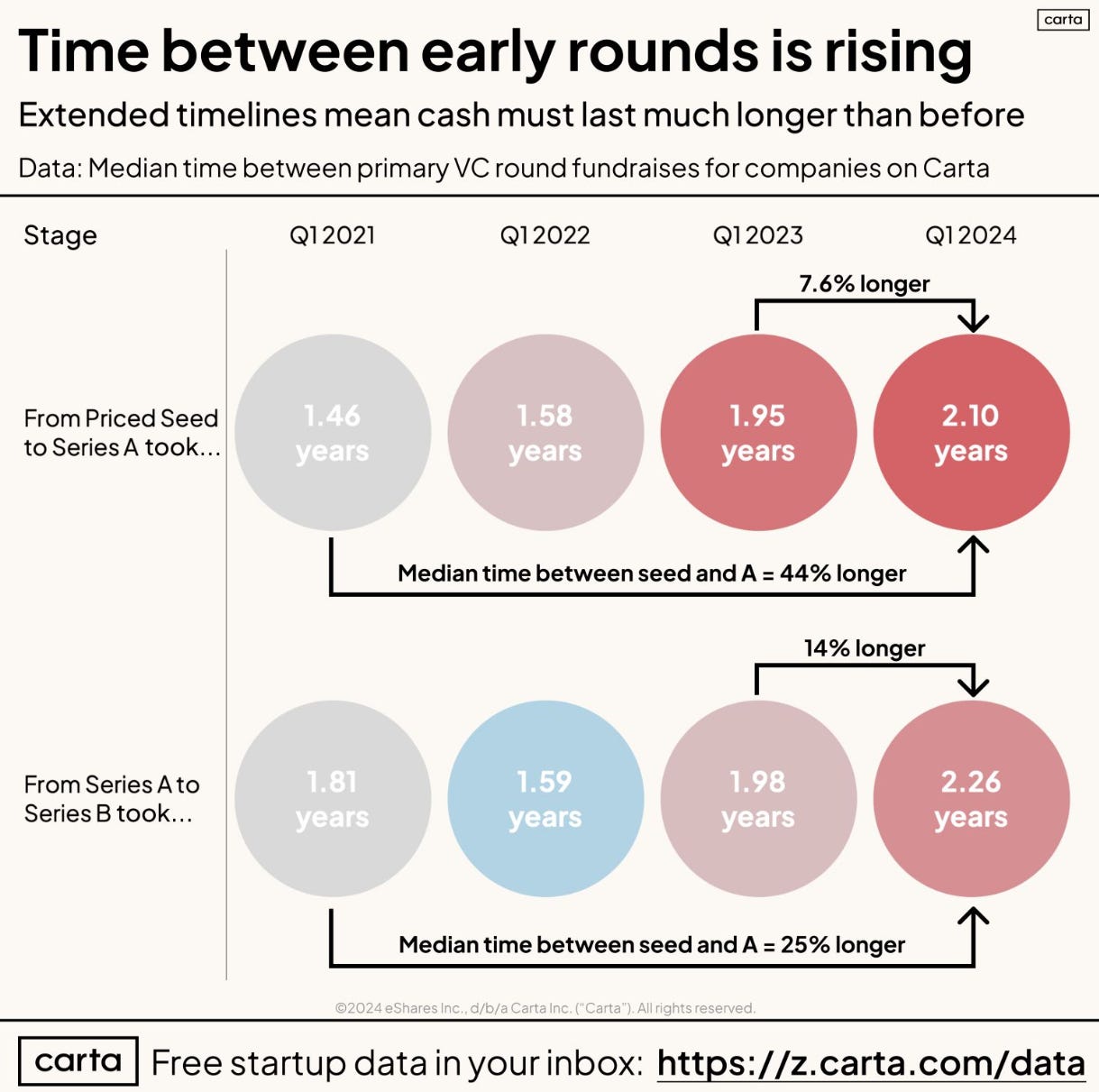

A couple months ago he had shared that the time from Seed to A and A to B was taking 44% and 25% longer respectively in this market, now over 2 years for both (below).

The natural question that came up for me was “how long does it take to get to seed?” This is a hard one to come by because founders will do a lot of weird things to get a company started, predominantly give their rounds weird names and stack SAFEs at varying valuations and check sizes, cobbling together enough capital to build something worthy of an early stage fund taking them seriously.

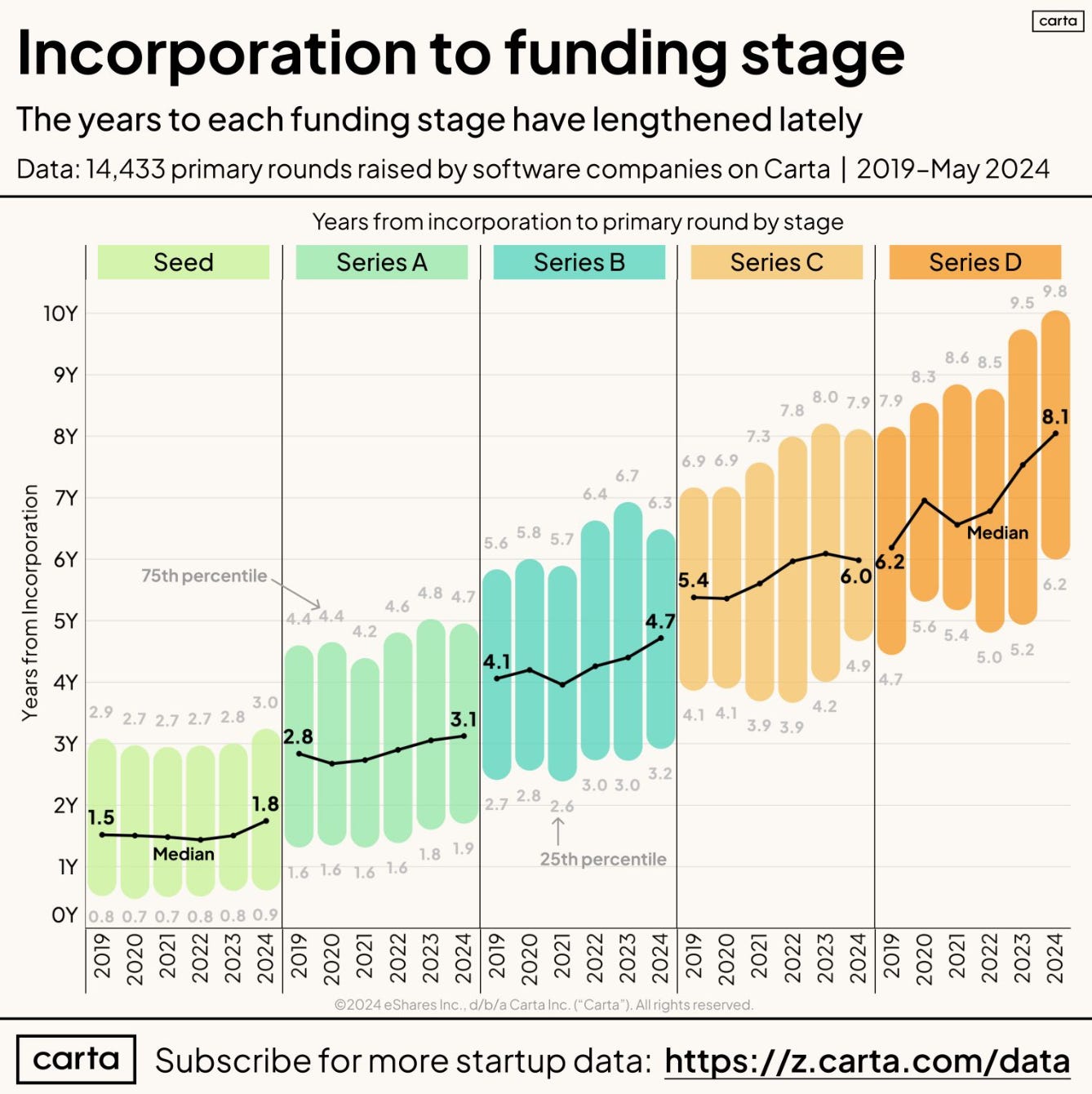

We came up with an idea to measure these rounds from time of incorporation. Unsurprisingly to those who know “early stage” well, the data showed that it’s taking 1-3 years to make it to a priced seed round (below), and instead of becoming easier, it’s actually taking longer—just like Seed to A and A to B.

That means that founders, from the moment they incorporate, are wandering through the founder journey for 12-36 months, raising capital where they can, building what they’re capable of with limited resources, and attempting to prove demand, all before a seed fund will actually lead a round.

So then I was thinking, “but what about before incorporation?”

And I asked a few founders, “how long were you seriously talking about and tinkering with starting a company before filing for incorporation?”

Answers ranged from six months up to many years. You see, founders aren’t just having an epiphany one day, turning their current careers on their heads, dropping everything in their personal lives, and filing for incorporation. Instead, they’re being thoughtful about what it takes, the risk involved, the time commitment, the quality of the team they can build, and their confidence in the idea and the market.

We call this the inception stage.

Inception stage includes this six to twelve month journey of getting serious about being a founder.

And it also includes the first 12 of 36 months that the Carta data shows it takes before an early stage VC will take you seriously.

But it gets even crazier.

Across 23,241 companies between 2013 - 2019 who participated in accelerators, the average company age was 3.1 years old, and revenue was $114,437.

That means founders are typically spending up to 3 years to be taken seriously by an accelerator, let alone a seed fund, and they’re taking up to 7 years to build a Series B company:

6-12 months from inception to incorporation

12-36 months from incorporation to acceleration

12-36 months from Seed to A

18-36 months from Series A to Series B

The faster moving companies can get there in 3-4 years total, but it’s rare, particularly when including inception—the months before the company is officially filed as an entity.

I bring this up because it highlights a major gap in venture capital, and a rate-limiting step for exceptional people starting world-changing companies.

Those first 6-12 months of inception are wrought with loneliness, uncertainty, lack of resources, and tremendous pressure.

If accelerators are working with companies who are 12-36 months old and revenue generating, then who is helping the inception stage founders?

Who is building community at day zero to help founders find co-founders and first employees?

Who is building a system to underwrite these founders before they’re deemed accelerator ready? Or better, yet, who is helping these founders skip over the accelerators altogether?

Who is reducing the burden and responsibility of taking institutional money so that you can use that inception stage time to truly figure out if what you want for yourself and for your future is to be on the venture treadmill?

The problem and the reason accelerators and early stage VC’s come into these companies so far into their journey is because there’s too little to underwrite. It’s perceived as too risky to simply back a founder when there’s no product, team, or revenue to point to.

But that’s also a major opportunity. It’s an opportunity for funds like Antler to create massive yet highly selective founder communities all over the world where equity and cash is not exchanged up front, and where value is provided to founders first and foremost, and in return the fund has an opportunity to underwrite execution and leadership rather than ideas and markets.

As I’ve written about before, the math of inception stage is misunderstood too.

Inception stage is mispriced because it has the hit rates of accelerators (2-6%), with the fund-through rates to seed (50-70%) that produce systematic alpha.

In fact, fund of funds strategies are becoming increasingly popular due to their diversification—putting 100+ seed stage companies in a portfolio for example. But inception funds produce a similar diversification by investing in 200+ companies and graduating 50% to seed. The difference is that the entry points are materially lower than fund of funds, $1m-$3m as opposed to $8m-$20m, which in turn adds a multiple onto that upside created by the larger portfolio.

Think about it. If you invest in 200 companies at a $2.5m valuation and 50% make it to seed, then it’s as if you invested in 100 companies at a $5m valuation. And with average seed stage valuations hovering at $13m in the US, that’s a systematic $8m alpha (2.6X multiple) created by the delta in valuation relative to fund-through.

Said differently, would you rather start with 25 companies in a seed fund marked at 1x, or start with 200 companies, but end up with 100 seed stage companies in a fund already marked at 2.6x?

I could go on and on, but that’s what’s on my mind this week.

See you Monday.

Continue to be excited to see you and the Antler team closing those gaps in support for inception-stage founders

Jeff - following my weekend thoughts on early stage funding https://www.linkedin.com/posts/elliotgrossbard_startup-vc-funding-activity-7216114765352312836-WqlR? this entry really had me asking some of the same questions you included. Learning more about Antler and the crucial part it plays in a startup and founder's journey opened my eyes a bit wider