Fund of Funds vs. Inception Funds: The Better Bet?

A deeper look at inception

TLDR: Looking at fund of funds vs. inception funds on diversification, price, fees, and liquidity. FoF’s predictably produced ~2.5x while Inception produced ~3x-5x.

For years, LPs have been sold on the diversification and "access to top managers" pitch that underlies most fund of funds (FoF). And to be fair, FoFs are one of the most underappreciated products in venture. They offer access, scale, and a smoother ride through volatile markets. In fact, many studies, like this article from Pattern Ventures last week, show that FoFs often outperform LPs who try to pick individual funds.

But there's a quiet countertrend rising: inception funds, and they’re not often discussed in the same conversation. If you believe that early entry, founder proximity, and portfolio efficiency drive real venture outcomes—you might find yourself asking whether FoFs are as good as it gets, or if there’s something mathematically stronger?

The Core Hypothesis

FoFs are overlooked and underrated. But inception funds may be mathematically even stronger—offering lower entry prices, more uncorrelated diversification, and structurally higher upside optionality.

Let’s unpack both sides—with data.

1. Fee Stack: The Double Tax Problem

Fund of Funds deliver strong risk-adjusted outcomes—but pay for it in fees:

1–2.5% management fee and 10–20% carry to the FoF

Plus the same 2/20 structure to each underlying fund

Many still deliver 1.8x–2.5x net, which beats most individual LP portfolios.

Inception Funds are ~10% less:

Most all inception funds front-load with higher fees during deployment, either with a higher percentage early or a per-deal fee

Even still, total fees often net to 18-25% of a fund vs. 30%+ for FoF

Historical inception-stage funds often reach 3x–5x net multiples when they capture even a handful of outliers.

2. Entry Price: Buy Low or Buy Late

FoFs give access—but often post-first-close:

Valuations already marked up ($15-30m post-money)

Lower ownership per dollar

Inception Funds buy earliest:

Day Zero pricing ($1.3m - $2.5m)

Own more for less

In the case of most seed and series A funds, they are aiming to buy 10-20% ownership for $1-5m of LP capital. In the case of inception funds, they are owning ~10% for $500K.

Take the YC example:

$125K for 7% = $1.78m valuation

$375K on uncapped MFN, converting at an average of $14.4m = 2.6%

9.6% average ownership for $500K

In this lens, YC, though more of an accelerator than an inception fund, is deploying 50-90% less capital per company and owning the same amount, meaning they can afford higher diversification for the same fund size.

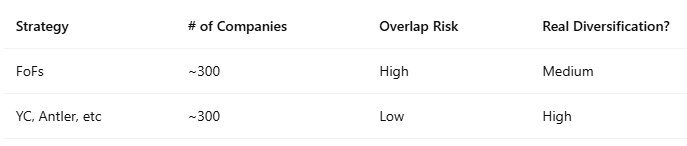

3. Diversification: Real vs Theoretical

FoFs offer real fund-level diversification—but the portfolios often overlap. The illusion of scale can mask concentration.

Inception Funds diversify at the company level:

100s of distinct cap tables

Spread across geographies and themes

Less correlated exposure to the same 20 “top” GPs

4. Return Dispersion: Smooth vs Spiky

FoFs win on consistency. They mitigate downside, manage risk, and reduce volatility. Great for institutions with strict return targets.

But Inception Funds chase convexity:

A single Stripe, Airbnb, or Coinbase can 10x a fund

Power-law outcomes happen earlier, with 100x - 1000x happening pre-IPO

Selling portions of their positions to growth equity rather than waiting for exit

5. Portfolio Construction: Example Breakdown

Fund of Funds – $100M FoF

$5M in 15-20 funds

20 companies per fund

300-400 companies, often overlapping

Strong fund access, but diluted alpha

Reserves for fees, and sometimes direct investing

Inception Fund – $100M Day Zero

200–400 companies at $125K–$300K checks

Substantial reserves for follow-on and pro-rata protection

High ownership at low cost, high diversification

Cap table optionality for pre-IPO liquidity

6. YC vs Fund of Funds: Real Performance Data

YC (2022 data):

Internal IRR: ~30–35% gross

Net TVPI: 4x–6x for early batches

Portfolio: 4,000+ startups, 80+ unicorns

Typical FoF:

Net IRR: ~8–14%

Net TVPI: 1.8x–2.5x

Smoothed returns, less tail risk

7. Capital Flow Trends

According to Deloitte, the number of family offices has grown from 6,130 in 2019 to 8,030 in 2024, with projections reaching nearly 11,000 by 2030. Similarly, aggregate family office AUM is expected to grow from $5.5 trillion today to $9.5 trillion in 2030, a massive $4 trillion increase in just the next five years! (Pattern Ventures)

As capital flowed aggressively into family offices during ZIRP-era, and in turn, into fund of funds products for their high diversification and predictable DPI, more emerging managers have been able to get funds off the ground.

However, this more recent narrative that FoFs are the best institutional grade venture product really lacks the full exploration of the innovation economy and where asymmetry exists.

If you’re searching for diversification, inception funds are similar or higher.

If you’re searching for low entry prices, inception funds are more disciplined.

If you’re searching for meaningful ownership, inception funds are similar.

If you’re searching for Power Law pre-IPO exit liquidity, inception has it.

In total, fund of funds are a fantastic product—they deliver access, smoother returns, and real diversification. For LPs who want reliable, scalable exposure to venture, FoFs may be a great option. However, mathematically, inception funds are built for upside. They compound early. They diversify broadly. And they capture the kind of asymmetry FoFs can’t always reach.

It doesn’t have to be either/or, but for LPs willing to lean into early-stage complexity, the future might be built closer to the cap table.

See you Monday.

So, Inception investing at this scale is real? You only imagine friends and family, and nowhere near the figures mentioned here. Do we have success stories or at least recent investment news?